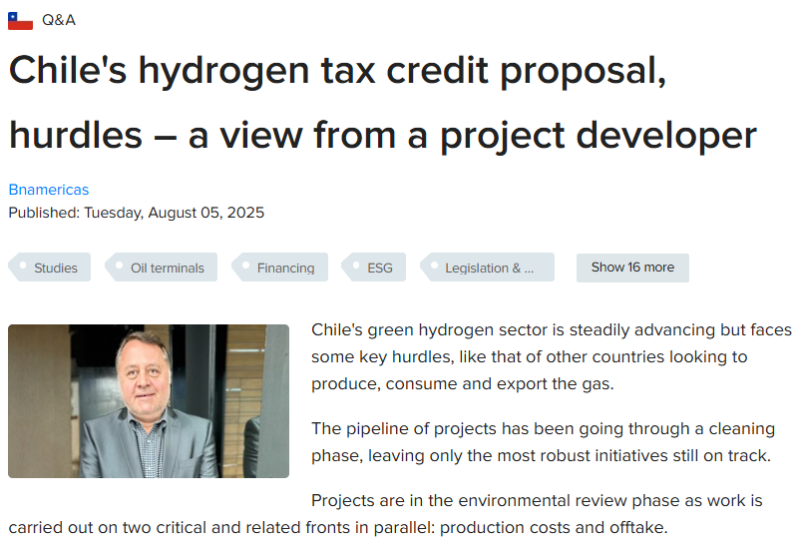

Chile’s green hydrogen sector is steadily advancing but faces some key hurdles, like that of other countries looking to produce, consume and export the gas.

The pipeline of projects has been going through a cleaning phase, leaving only the most robust initiatives still on track.

Projects are in the environmental review phase as work is carried out on two critical and related fronts in parallel: production costs and offtake.

To help get projects underway and unlock the country’s vast green hydrogen and derivatives potential, the government said it would propose a US$2.8bn tax credit plan via a bill.

To obtain a view of the situation from the supply side, BNamericas speaks to Juan Guillermo Walker, CEO and founder of developer FreePower Group. Walker also provides an update on company projects planned for the Magallanes and Antofagasta regions.

BNamericas: What aspects of the government announcement stand out for you?

Walker: What stands out is the amount committed to promoting the green hydrogen industry and its derivatives, particularly focused on stimulating demand. The current issue isn’t the production of hydrogen, synthetic fuels or ammonia, but rather the lack of demand. Supply has advanced much faster than consumption, mainly due to cost issues.

Today, even if we wanted to replace all the hydrogen and ammonia used globally with green alternatives, the capacity of current projects would still be very limited. The main challenge lies in the cost gap: producing one ton of ammonia with green hydrogen is significantly more expensive than doing so from natural gas. Conventional ammonia can cost between US$300/t and US$400/t, while green ammonia can easily exceed US$600/t or US$700/t, and some projects even struggle to get below US$1,000/t.

That price gap makes the industry unwilling to replace a high-carbon product with a cleaner one, simply because the cost is much higher. Let’s remember that the global ammonia industry, which moves around 200Mt/y [million tonnes per year], represents approximately 2% of global greenhouse gas emissions. This is because the hydrogen used in its production comes from natural gas through processes that release CO2.

So, there are two options: capture that CO2, which makes the process even more expensive, or use electrolysis powered by renewable energy, which has a very low carbon footprint but remains a costly and energy-intensive technology. It takes between 50kWh and 55kWh per kg of hydrogen, which is still high.

In that sense, although I appreciate that the government is proposing mechanisms like tax benefits to help companies sell their products, I don’t believe that addresses the root of the problem. If I were in charge of promoting this industry, I would prioritize funding for research and development. [State development agency] Corfo, for example, already has instruments like the innovation and development funds (FID), and these could be complemented with multilateral banking or direct state investment.

Why? To license more efficient technologies or develop our own solutions that would allow, for instance, the production of ammonia directly from nitrogen and water, without going through hydrogen as an intermediate.

The focus must be on reducing energy consumption in hydrogen production. If we can reduce consumption from 55kWh/kg to 30kWh/kg, we could lower the cost from US$4/kg to just US$2/kg – a radical shift. The same applies to ammonia synthesis and synthetic fuel production, where there is also room for innovation.

Another key point is the cost of using the electrical system. In the north of the country, if I produce hydrogen connected to the national grid, I have to pay system charges, which can reach US$15/MWh. Even if the energy is free, those charges make me lose competitiveness. Therefore, just as energy for strategic reserves is exempt from system charges, the same could be considered for hydrogen projects.

In addition to everything mentioned above, technological development and the reduction of systemic costs, it’s important to promote the use of shared infrastructure. If I partner with [state oil company] Enap, a port, or another company to use existing facilities, there should be tax incentives for that type of collaboration, which avoids duplicating infrastructure and helps reduce environmental impacts.

There’s no point in subsidizing demand if green products aren’t competitive compared to conventional ones. This is what happened with renewable energy in the beginning. Initially it was more expensive, but today it’s competitive thanks to innovation and economies of scale. Green hydrogen should follow the same path.

Providing subsidies to buyers won’t work if these products remain economically unviable. We must first improve the product’s competitiveness. Then, it does make sense to think about stimulating demand in sectors like blending with natural gas, use in refineries, or in the chemical industry.

In the case of ammonia, there are clear uses in mining explosives, fertilizers or maritime fuel, where there is already concrete progress with vessels that could run on ammonia.

BNamericas: As a developer of projects in Magallanes region, how big of an impulse could this give to green hydrogen in Chile? Could it, for example, trigger final investment decisions?

Walker: Measures like incentives for shared infrastructure, streamlining of permits and public-private coordination around key enablers could be decisive for progress.

It’s not just about building plants but also ensuring their long-term operation. This requires roads, infrastructure, water, services and territorial planning. In areas like Magallanes, outside of Punta Arenas, Porvenir or Puerto Natales, many localities are quite underdeveloped and lack basic infrastructure. This presents an opportunity to revitalize communities that were left behind after the decline of the oil and gas industry and turn them into development hubs.

BNamericas: What’s the state of play regarding your two Magallanes green ammonia projects, Cabeza de Mar and Frontera?

Walker: Both projects have completed, or are about to complete, their environmental baseline studies. Cabeza de Mar will likely be the first to move into more definitive stages and begin engineering. Frontera will follow with a slight delay.

Specifically, we expect to submit the Cabeza de Mar project to the environmental impact assessment [EIA] system within a year. At the same time, we’re refining aspects such as the import and export strategy, port development and the modular architecture of the project, which makes it more flexible but also requires key decisions.

For Cabeza de Mar, engineering will likely start after September, and the EIA will be prepared toward the end of the year. Frontera, by contrast, is about a year behind Cabeza de Mar.

BNamericas: What about Punta Patache in Tarapacá region?

Walker: Punta Patache is a very interesting project. It’s located in an area that’s less saturated than Mejillones but already developed, which makes it easier to move forward. There used to be a coal-fired power plant there that has been dismantled, and there are two ports handling copper concentrate and filtration plants.

We’re evaluating the use of industrial wastewater as a water source for the process, which would be very positive from an environmental standpoint.

Check out the interview here: bnamericas